These types of claims and

commercials have become so prevalent that both the IRS and

the Consumer Financial Protection Bureau are considering

oversight of this portion of the financial services

industry.

Concerns have developed based

on requirements of large up front fees and frequent

failures to settle debts based on promised terms. BEWARE!!

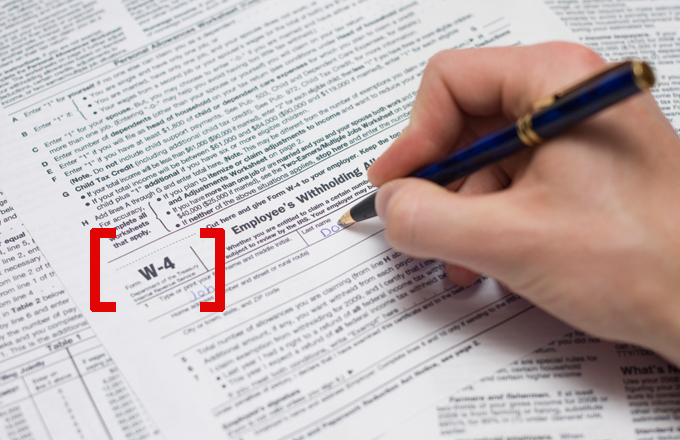

You will fill out a Form W-4

when you begin a new job. Additionally, each time you

experience a life change such as a new address, marriage or

a babys birth, you need to update your W-4

promptly.

Do not wait until the end of

the year as you may experience an unpleasant surprise in how

much you owe in taxes. If you have problems with the

form your HR staff can help you. You can also contact your

tax accountant for assistance.

Any portion of the federal tax

due and unpaid as of the payment due date and the return is

filed after the filing date is subject to a late filing

penalty.

The penalty is 5% for each

month or part of a month that the tax return is late, up to

a maximum penalty of 25%.

If you file your return more

than 60 days after the due date or extended due date, the

minimum penalty is the smaller of $135 or 100% of the unpaid

tax.

A tax extension is a way to

ask the Internal Revenue Service for more time to file a

tax return. The deadline to file your tax return is

normally April 15th. By filing Form 4868

you can extend the deadline by six months to October 15th.

However, the extension of

time to file is not an extension of time to pay. The

payment for your taxes is still due on April 15th.